Introduction

In the past few decades, aquaculture is the fastest growing agricultural field in the world, and will continue to maintain its growth momentum, providing more abundant food and nutrition for the world population.The fishery economy is an important part of Chinese economy. According to the China Fishery Statistics Yearbook published by the Ministry of Agriculture and Rural Affairs of China, China is the biggest aquaculture country in the world. In 2022, the output of aquaculture will be 5.57 × 107 t, accounting for 81.1% of the total output of aquaculture in China and about 60% of the total output of aquaculture in world. However, the fishery in China is currently facing some problems, such as unbalanced development, relatively extensive farming and fishing, and low quality and benefit. This shows that although China is a big aquaculture country, it is not one of them, and there are still bottlenecks to overcome. High quality development has become an urgent need.

Fishery listed companies are not only a combination of listed companies and fishing companies, but also a link between fishermen and the market. As a leading enterprise in the aquatic products industry, listed fishery companies represent the development level of aquatic products industry in China to a certain extent, and its development has become the key to promoting the development and industrial upgrading of chinese fisheries economics.

In recent years, the financial scandals of fishery listed companies have been increasing, and Lantian Co., Ltd. (836579), which is mainly engaged in aquaculture, was forced to withdraw from the market due to fraud. Zhangzidao (002069) is also notorious for the financial fraud incident of “scallop fleeing”, and Wuchang Fish Co., Ltd. (600275) has been labeled as “demon stock”, “protecting shell” and “delisting” for many financial violations. Due to huge losses and declining profitability, the Oriental Ocean Co., Ltd (002086). has also been marked as ST. The fishery sector is constantly thundering, and the phenomenon of financial data “fraud” is serious. The reason is that the management concealed the bad financial situation to meet the expectations of the third party. As a basic indicator to measure the performance and development ability of fishery companies, financial performance has attracted much attention from stakeholders. Whether the management of fishery enterprises discloses real financial performance or adopts fraudulent behavior of financial fraud, it will hit the confidence of investors and affect the healthy development of the fishery market. Besides China, financial issues in the fisheries sector are a significant concern in other countries as well. In Bangladesh, for example, poor governance has led to the deterioration of the sector’s financial condition.1 Similarly, in developed countries, financial problems persist. Some European fisheries companies have been found to evade regulations by misreporting catch volumes and falsifying financial data.2 So how to help fishery listed companies achieve stable financial performance and sustainable performance growth has become the “salvation way” to solve the above problems.

Scholars have conducted extensive research in the field of fishery economy, attempting to interpret the operational performance and economic benefits of fisheries from the perspective of economic management. A study approached the issue of fund management from the perspective of operating funds of fishery enterprises using qualitative research methods, and proposed solutions to such problems.3 Some studies use regional constraints, for example, using Shandong Province in China as the main sample, to analyze the cost-benefit structure of small and medium-sized scallop farmers.4 Existing research compares the financial performance of tuna long-term fisheries in Japan and Australia through a horizontal comparison method, and analyzes the main drivers for improving the profitability of the tuna industry.5 Scholars have also analyzed the fishery product service portfolio that maximizes total revenue from a more microscopic perspective using a multi species fishery model.6 In the study of macro samples, previous researchers used regression analysis to reveal the relationship between the social responsibility performance of fishery enterprises and their financial performance.7 Some scholars adopt a more macro perspective and use panel data regression to analyze the impact mechanism of vertical integration in fishery enterprises on their performance.8

From the above literature review, it can be seen that research on fishery economy has spanned from a micro perspective of sub dividing regions and types of aquatic products to a macro level of the entire industry, and countless research methods have been used in this regard. To sum up, the research methods for fishery economy can be roughly divided into two categories: qualitative and quantitative. However, most scholars use quantitative analysis methods, such as regression analysis, to make quantitative research in this field. Rich research results have been accumulated on single causal relationships. However, the financial operation activities of enterprises are complex and dynamic events with uncertainty and complexity. There is a non-linear interaction between the various factors that affect financial performance, that is, the various elements of financial performance are interrelated and not independent responses. Regression analysis can only reveal the influencing factors and mechanisms of financial performance, but it is difficult to determine how the variables are related and combined and how they coordinate and play a role. However, for qualitative methods of studying fishery economic issues, there are problems with poor generalization and subjective inference processes, which may be difficult to generate practical significance.

Considering the deficiency of the above two research methods in the fishery economy, it is necessary to further study the complex driving factors of financial performance of listed fishery enterprises. Based on this research background, this study selected the listed fishery enterprises in China as the research object, and uses the fuzzy set qualitative comparative analysis method (fsQCA) to further explore the joint coordination effect between variables, which is helpful to make up for the shortcomings of existing research.

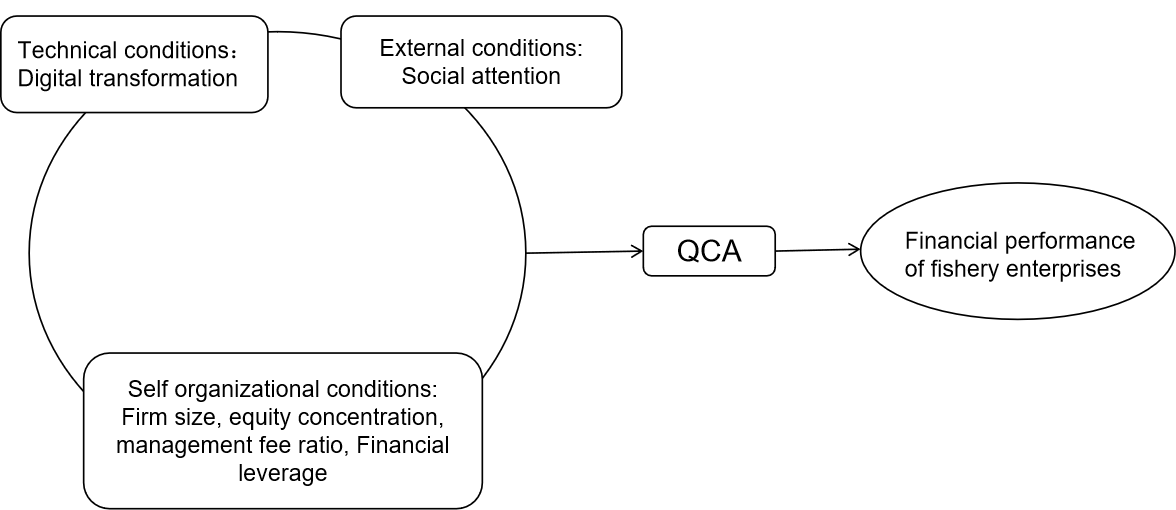

Theoretical analysis and research framework

Technical conditions of the enterprise

The Resource-Based View (RBV) posits that a company’s competitive advantage stems from its unique resources and capabilities.Technology is an important driving force and resource for company operations and industrial development. The maturity of aquatic technology directly determines the economic benefits of output.For example, the promotion of fishery technology has a significant promoting effect on the income of fishermen.9 Digital resources are an important direction for today’s technological development and a key factor in gaining technological competitive advantages in the current era.Digital capability is seen as an operational capability aimed at utilizing digital technology to enhance the operational efficiency of basic business activities.Based on dynamic capability theory, companies maintain competitive advantage in rapidly changing environments by continuously restructuring and utilizing internal and external resources.10 Digital transformation can help companies enhance their dynamic capabilities, adapt to market changes, and thereby improve financial performance.With the rise of the digital wave, the fishery industry has gradually joined the digital transformation, attempting to use digital technology to empower the operation and management of enterprises.11 Digital capabilities accelerate enterprise response, meet changing customer needs, increase revenue, and leverage digital technology to quickly organize enterprise resources and generate solutions, thereby gaining strong competitiveness.12 The improvement of digital application level in aquaculture systems has greatly promoted the level of aquaculture productivity.13 The smart fishing industry, which relies on digital technology, is a typical example of digital application in aquaculture and has become a sustained driving force for the development of the fishing economy.The popularization of smart fishing can not only improve the efficiency and benefits of fishing, but also protect the ecological environment and sustainable use of resources, which is of crucial significance for promoting the upgrading of the fishing industry and economic development.14

Multiple studies have demonstrated the positive effect of digital technology on corporate performance. However, few studies have focused on the linkage between digital technology and other factors that affect financial performance. Simply put, digital transformation can be linked to internal management, external attention, and other factors, collectively affecting a company’s financial performance. In addition, when a company lacks good external conditions or internal management defects, can digital transformation still produce configuration linkage effect and affect the improvement of financial performance?

Self organizational conditions

From an internal perspective, the organizational conditions of a company are one of the important factors that affect its financial performance. Overall, there is a positive correlation between the level of corporate governance and financial performance.15 The choice of different organizational and management modes by enterprises has different effects on finance. For example, the impact of equity concentration on corporate financial performance is positively correlated16 A study suggests that the relationship between equity concentration and corporate financial performance is an inverted “U” shape.17 However, when exploring the relationship between corporate governance and corporate financial performance, subsequent scholars selected Chinese manufacturing listed companies as research samples and found that the proportion of shares held by the company’s largest shareholder does not have a significant impact on corporate financial performance.18 Capital structure is an important reference indicator for companies in financial management. Scholars believe that capital structure has a significant negative impact on company performance.19 However, there are also studies that hold the opposite view: capital structure has a significant positive impact on company performance, that is, the higher the debt ratio, the better the company’s performance.20 The management cost of the enterprise runs through the whole production and operation cycle of the enterprise, and it is an important support to maintain the daily organization, operation and management of the enterprise. There is a relationship between the use efficiency of management expenses and the control of enterprise management cost as well as the overall management level of the enterprise.21

Previous research on the impact of equity concentration and capital structure on financial performance are inconsistent. This may be due to inconsistent industry types, company sizes, and internal management levels in the sample. The above factors can also influence and combine with each other, creating a synergistic effect on financial performance. Therefore, only exploring the impact of a certain management approach on performance has limited explanatory power. This article decomposes the organizational conditions of the enterprise into multiple elements and explores the linkage of these elements to enhance the explanatory power of the model.

External conditions

The enterprise is not an individual completely independent of the outside world, and its development is also affected by many external factors. Comprehensive governance of the government can play an obvious external role in the financial performance of enterprises. The implementation of incentive regulation by the government will provide some economic support to enterprises, and then improve their financial performance.22 Government regulation can regulate the daily operational activities of enterprises and constrain their behavior, thereby incentivizing enterprises to achieve the goal of improving their performance.23 In addition to the government, third-party independent institutions can also play an external role: external audit plays an important role in controlling and helping to quell agency conflicts, and helps to maintain the stability of enterprise financial performance.24

Based on the above analysis, there are two main ways in which external conditions contribute to financial performance, support and supervision.

In addition to the government and third-party institutions, the external influence on enterprises also includes a large number of medium and small investors, media, competitors and other broader subjects. Social attention is a general concept, which includes the attention of all kinds of stakeholders to the company, so its external role can not be underestimated.Specifically, the attention of investors is conducive to expanding financing channels, alleviating financing constraints for enterprises, and thus changing the financing structure of enterprises.25 The attention of consumers indicates that the increase in corporate awareness is beneficial for opening up sales channels for the company. But at the same time, it will also play a supervisory role on the enterprise, affecting its management methods and financial performance.26

In the era of big data, the “spotlight effect” of enterprise digital technology has brought high social attention. And social attention is clearly expected to have a supportive and supervisory effect on the changes in the company’s own organizational conditions. So the three may have a linkage effect, jointly affecting the financial performance of fishery enterprises.

Research framework

TOE(Technology-Organization-Environment)is a comprehensive analysis framework for technology applications, suitable for classifying and exploring complex causal relationships. This framework has been widely applied in fields such as psychology, economics, and management.The impact of the linkage between technology, organization, and external environmental factors in this study indicates that it is necessary to explore the complex linkage phenomenon of fishery financial performance based on this framework.

In a word, the way to achieving high financial performance of fishery listed companies is influenced by three basic factors: external conditions, organizational conditions and technology. It is difficult to improve the operating performance of the enterprise by a single factor alone. Therefore, this paper decomposes these three factors into six conditional variables, and analyzes whether the existence of a single factor is a necessary condition for fishery enterprises to achieve high performance by using FsQCA method. Based on above analysis, this reaserch continues to explore how many factors can synergistically affect the improvement of the operating performance of fishery listed companies. The specific research framework is shown in Figure 1.

Research design

Research method

Qualitative Comparative Analysis (QCA) is a method that studies the complex relationships between different factors and their outcomes. It is particularly useful for case studies involving small to medium-sized samples, unlike traditional methods, which might struggle with such sizes.

QCA stands out because it can handle the detailed and intricate nature of business management, where financial performance is affected by many interacting factors. This approach considers the whole picture rather than isolating individual factors, making it excellent for understanding the multiple reasons behind financial performance. QCA uses three types of sets to classify data: clear sets (for yes/no or either/or situations), fuzzy sets (for situations with a range of possibilities), and multivalued sets (for multiple categories). This flexibility allows it to handle different types of data comprehensively.

Financial performance isn’t just a simple matter of having or not having certain factors. The QCA method, especially the fuzzy set version (fsQCA), can analyze combinations of multiple factors simultaneously, making it a powerful tool for understanding the complex dynamics that influence financial performance in companies. The specific reasons for using QCA method to explore the financial problems of fishery listed companies are as follows:

-

In order to reveal the formation path of financing risk of fishery enterprises, it is not enough to take one enterprise as a case, it is necessary to consider the situation of representative enterprises in the whole industry. The core business activities of fishery enterprises are different, and the financial situation is complex, resulting in different degrees of financial performance.FsQCA can analyze the multiple causality leading to a given result by forming a combination of logical conditions, identifying necessary and sufficient conditions, exploring the equivalent and opposite situations, and analyzing the sensitivity of the condition configurations in which the results exist or do not exist.27

-

The number of listed fishery companies in China is insufficient, and the sample size is too small to be suitable for traditional regression analysis methods. However, the QCA method is appropriate for studying small samples.

-

The operation of financial systems is intricate and not determined by a single factor. In practical situations, it is often the combination of multiple factors that leads to changes in financial performance. Therefore, QCA can better simulate the dynamic configuration of various factors in practical situations. Additionally, fsQCA does not require independence between variables, nor is it affected by autocorrelation or multicollinearity. It is suitable for a unified framework study of multiple independent variables.28 FsQCA assists in comprehending the diverse driving mechanisms behind common outcomes in various scenarios, and further examines the compatibility and substitution relationships between conditions.

Data sources

This study selected listed companies related to the fishery industry in A-shares from 2011 to 2022, removed ST companies and ST * companies in the selected regions, and removed samples with missing or abnormal data. After the above screening, 102 sample observations were finally obtained. Most of the financial data required for this study for listed companies comes from the CSMAR database. Specific variable measurements can be found in the following text and Table 2.

Variable measurement

Digital transformation: Currently, the digital transformation of enterprises is an important strategy for high-quality development, and this type of characteristic information is more easily reflected in annual reports with summaries and guidance. We refer to the research methods of Fang and Liu (2024).29 This article measures the word frequency of the core underlying technical architecture that constitutes the digital transformation of enterprises in the annual reports released by listed companies as a proxy indicator for enterprise digital transformation. First, we collect and extract relevant content from the annual reports of listed companies from 2011 to 2022 through Python crawler functionality. Secondly, build a text vocabulary library for enterprise digital transformation, expand vocabulary to Python’s jieba library, remove pauses, and count the number of times vocabulary appears; To reduce right skewness, the keyword frequency of each listed company is summed up and logarithmically processed to measure the degree of digital transformation of each enterprise.

Financial performance:At present, return on total assets (ROA) and Return on Equity (ROE) are commonly used in academic circles to measure the financial performance of the industry. ROE stands for return on net assets and measures the return on investment of shareholders; ROA is the return on assets, which measures the level of return on investment enjoyed by shareholders and creditors. The goal of corporate finance is to maximize shareholder 'equity, so ROE indicators is more useful. Therefore, this article uses the return on equity to measure financial performance.

social attention:With the development of information technology and internet technology, it has become a common behavior for individuals to use search engines to obtain company information. Many scholars have made use of Google search data to carry out theoretical research on external concerns. In China, Baidu search is in a dominant position in domestic search engines, and most individuals usually use Baidu search engines to search for information about investment objects, so Baidu index is more representative. This paper refers to the research of Zhang and Fang (2014),30 and uses the Baidu index of enterprises during the sample period to measure the intensity of social concern. This value represents the degree of social concern, and the greater the value, the higher the degree of concern.

Other variables:Firmsize:according to the measurement method of previous research, this paper selects the logarithm of total assets as the index to measure the enterprise scale.

Management fee rate,Proportion of management expenses to current year’s operating income. The higher the management fee rate, the higher the management expenses used by the enterprise in that year.

Equity concentration is the quantitative indicator of whether all shareholders exhibit equity concentration or equity dispersion due to different shareholding ratios. This article evaluates equity concentration using the shareholding ratio of the largest shareholder.

Financial leverage reflects a company’s capital structure, and our study measures it by the ratio of year-end total liabilities to year-end total assets.

Data calibration

Data calibration refers to the process of belonging to a set of cases.There are three existing data calibration methods, namely direct allocation, direct calibration and indirect calibration. The direct calibration method is the most common and formal calibration method. On the basis of referring to related research, this paper uses direct calibration method to set the 95th percentile, median and 5th percentile of sample data as completely subordinate, intersection and completely non-subordinate anchor points. When the fuzzy membership degree is 0.5, there will be the problem of configuration attribution. In order to avoid the above problems, the constant 0.01 is added manually in this article. The results of fuzzy set calibration and descriptive analysis are shown in Table 3.

EMPIRICAL ANALYSIS

Correlation analysis

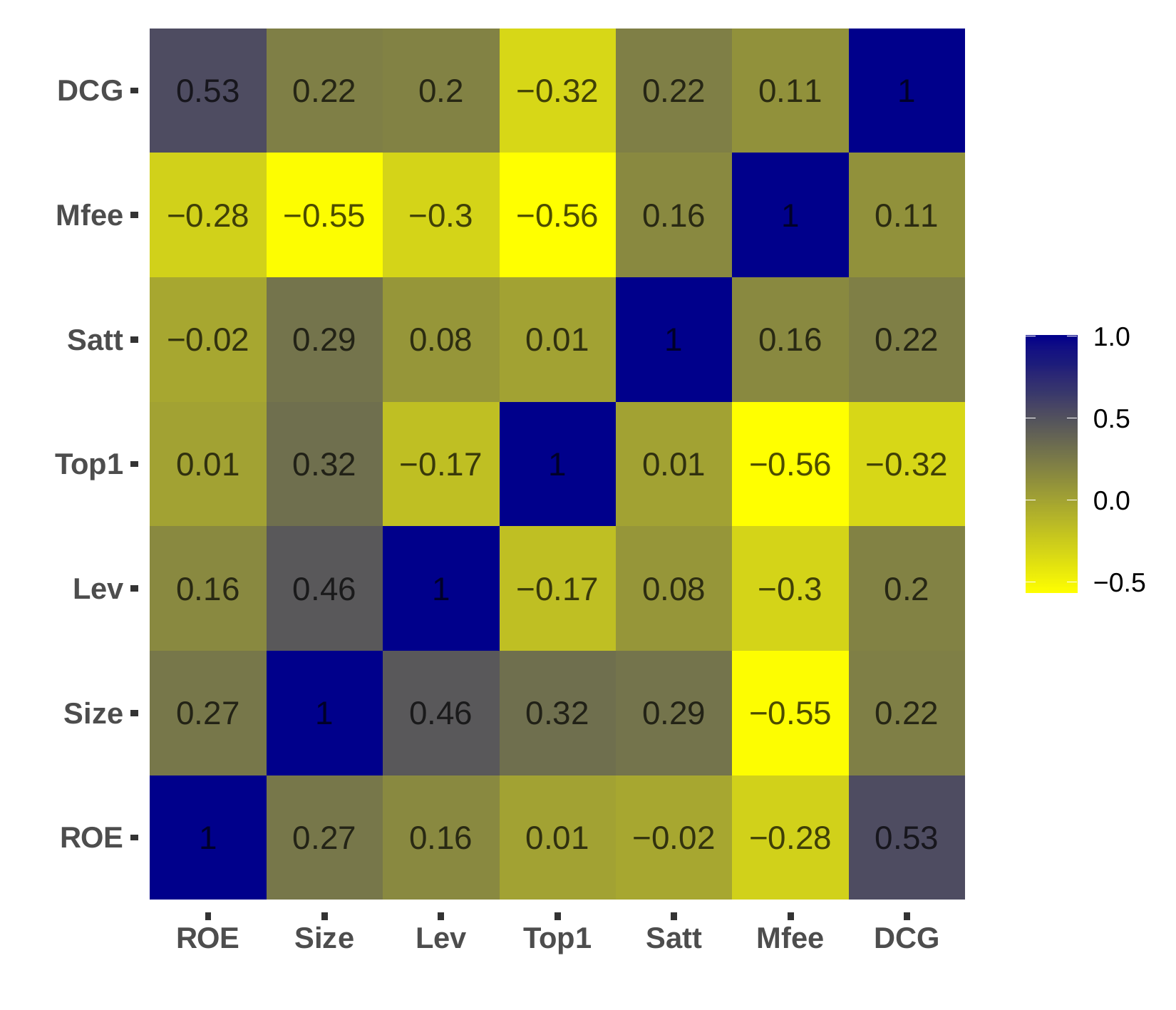

Before conducting the formal empirical test, this paper first performed a correlation test between variables. Correlation analysis can help researchers identify and understand the potential relationships between different variables in advance, providing preliminary evidence for subsequent causal analysis.

Using R tools software, a heatmap of correlations between variables was drawn (Figure 2). The results show that digital transformation, company size, and management expense ratio have relatively significant correlations with financial performance. However, the remaining three conditional variables do not have particularly significant correlations with financial performance. This indicates that the relationships between the three conditional variables and financial performance may be non-linear, requiring further qualitative comparative analysis to explore the impact of internal governance mechanism combinations on corporate innovation investment.

Necessary condition analysis

According to the research steps of the fuzzy set qualitative comparative analysis method (fsQCA), before further analyzing the data, it is necessary to verify whether there is a single conditional variable that is a necessary condition for the occurrence of results. If the consistency of a single condition is below the threshold of 0.9, there is no necessary condition for the result to occur.

According to the setting of fsQCA 3.0, adding “~” in front of the variable means it does not exist. As shown in the Table 4, the necessity test value for no single variable is greater than 0.9, which indicates that there is no core situation leading to high or low financial performance. Therefore, this article will explore the adequacy effect of configuration paths from the perspective of variable combinations.

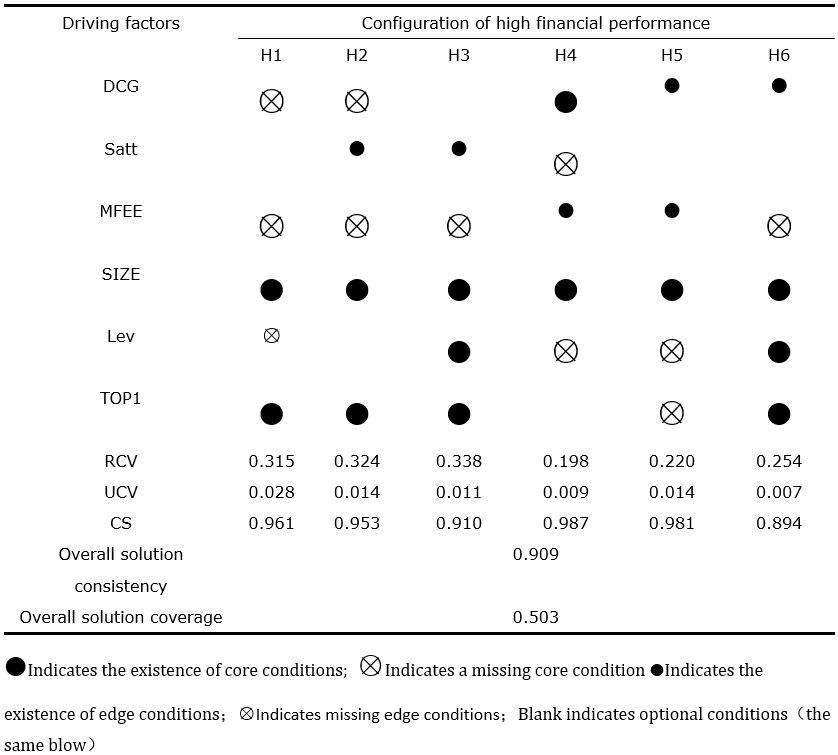

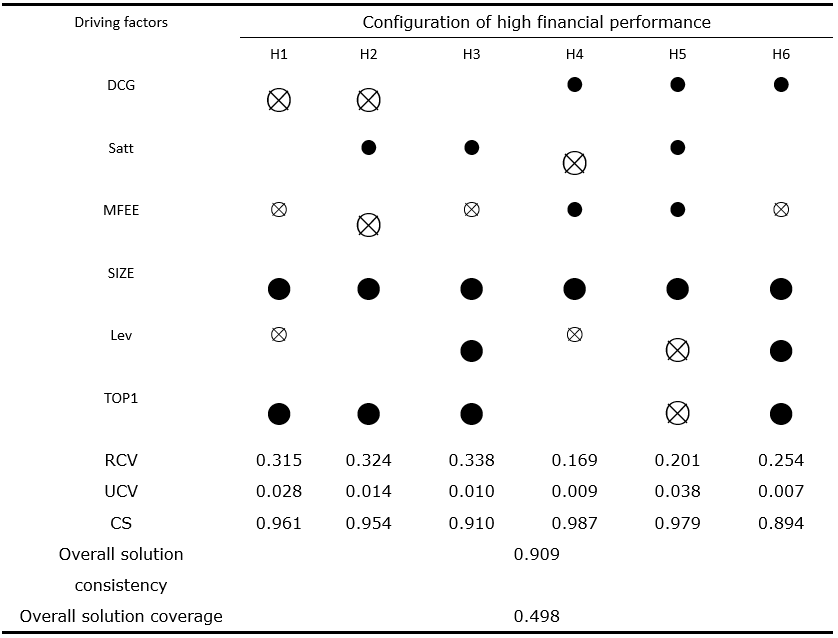

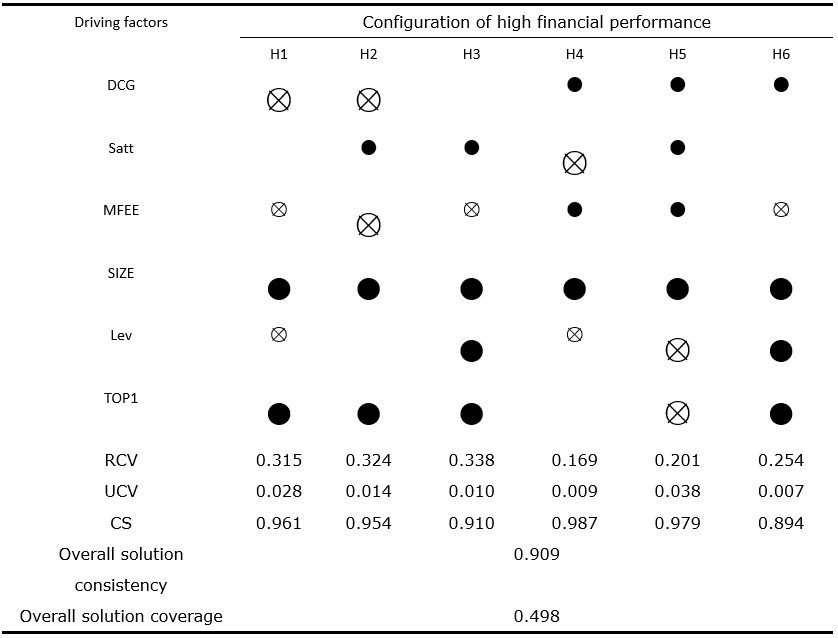

Configuration analysis

Using fsQCA3.0 software for element linkage analysis, this article sets the original consistency threshold to 0.8 and the PRI consistency threshold to 0.7. Configuration analysis was conducted on the multiple antecedent factors that led to the results, resulting in simple solutions, intermediate solutions, and complex solutions. On the basis of referring to existing literature on conditional partitioning, this study mainly uses intermediate solutions and uses simplified solutions as an auxiliary to establish configuration configurations. The configuration partitioning is shown in Table 5, and there are 6 configurations with high financial performance. (H1, H2, H3, H4, H5, H6). The single configuration consistency levels of these six configurations are all greater than 0.8, and the overall consistency level reaches 0.910, far exceeding the standard of 0.8. The overall coverage of the model is 0.503, which is above 0.4. Six configurations explain why approximately 50% of fishing companies have high financial performance levels.

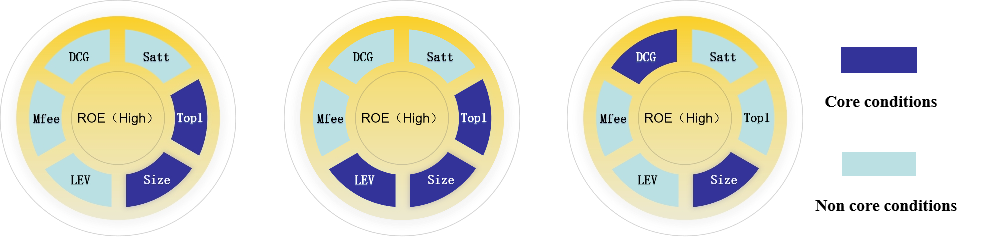

Organizational self driven (high centralization - high assets): Through horizontal comparison of various configurations, it is found that H1 and H2 have similar configuration structures: both have the same core conditions, with centralization and company size as the core conditions, which can be summarized as a high centralization+high asset organizational self pull configuration (Figure 3).When the proportion of shares held by the largest shareholder is relatively high, in order to maximize their own interests, they will be more proactive in their work, strengthen supervision of the enterprise, and thus promote the improvement of the financial performance of the enterprise.31At the same time, whether it is aquaculture or fishing, a large amount of funds are needed to invest in the purchase and maintenance of heavy assets. The larger the asset base, the larger the company’s scale, and the higher the economic benefits it generates. In addition, shareholder centralization and company size can have a linkage effect. In agricultural and fishery companies, the more concentrated the equity, the more favorable it is for improving investment efficiency. The controlling major shareholders of the company will find ways to effectively invest in the enterprise, which can better promote the improvement of investment efficiency and thus benefit the improvement of financial performance.32 Even in situations where technological and external conditions are relatively lacking in competitiveness, companies can still utilize centralized control by major shareholders and large-scale asset investments to achieve high financial performance. The representative case is Haida Group (002311), which has many controlling shareholders and a higher asset size than the industry average. At the same time, the profitability of assets is stronger in the same industry. This indicates that Haida has created relatively excellent financial performance through the combination of centralized management by major shareholders and increased investment in asset size.

Flexible and cooperative configuration (technology external organization): H3 and H6 have similar configuration structures, and both core conditions include companies with high centralization, large asset size, and a capital structure biased towards debt financing (Figure 3). Fisheries is a heavy asset industry, and production activities require abundant asset support, such as purchasing fishing boats, constructing fishing ports, and production sites for aquaculture. Asset size and returns are directly proportional for listed fishing companies, and investing in assets is an indispensable part of their production and operation. An increase in capital demand often accompanies the expansion of fishery assets, and the speed of debt financing is also relatively fast, which is a financing method that can help enterprises make quick responses. Therefore, a reasonable increase in the proportion of debt financing in the capital structure can effectively coordinate with the asset expansion strategy of fishery enterprises and thus have a positive driving effect on improving corporate financial performance. In addition, external social attention and digital transformation exist as marginal conditions for both configuration paths. This indicates that listed fishing companies can cooperate with digital technology innovation or strengthen social attention measures to achieve high financial performance. On the one hand, higher social attention can open up financing channels for companies, enabling them to obtain more financial support, optimize financing structures, dilute financial risks, and improve financial performance. On the other hand, it is also conducive to supervising and regulating the company’s daily activities, thereby motivating the company to achieve high performance.26 Digital transformation can also support centralized large-scale companies with high debt ratios. The reason is that digital transformation can bring about an improvement in investment efficiency.32 Digital technology can quickly identify signals from investment entities and improve the efficiency of identifying and handling risks, helping to reduce investment mismatches.33 So, while expanding the scale of listed fishing companies, they can also accurately allocate appropriate assets, effectively promoting the efficiency of fund utilization and helping to improve the company’s financial performance.

Dual collaboration type (technology organization): The configurations of H4 and H5 are similar, with enterprise scale as the core condition and digital technology as the core and edge conditions, respectively (Figure 3). This indicates that digital transformation has played an important role in these two configurations. This article categorizes these two configuration paths as technology-organizational dual-element collaboration. The higher the degree of digital transformation in large enterprises, the stronger the promoting effect on financial performance.34 Digital transformation may reduce costs and improve factor productivity by integrating production activities and financial management systems.35 Digital transformation can help companies achieve high financial performance goals despite high management expense rates. According to the truth analysis of QCA, the typical case is Shanghai KAI Chuang International Marine Company (600097), which is a large-scale ocean-going fishing enterprise, large fishing vessels needed for ocean-going fishing, aquatic products fresh-keeping, processing, storage facilities, communications, and fishing and navigation safety equipment, and high investment in fixed assets, accounting for about 35% of the total assets. In addition, it implements the digital strategy, uses digital technology to cooperate with production and management activities such as fishing and route operation, and provides digital technology support and guarantee for the realization of enterprise financial goals. ROE is stable at about 10%, leading to the average level of the same industry.

Robustness test

This article conducts a robustness test on the antecedent configuration of high financial performance. Firstly, keep the sample cases unchanged. (i.e., use the original samples for testing), Secondly, the frequency threshold of cases should be increased from 1 to 2. The results show that the generated configuration is consistent with the original configuration, and the coverage and consistency of each configuration and the overall solution remain unchanged (Table 6). On the whole, the conclusion of this paper is robust.

Results

This article summarizes six path configurations that help companies achieve high financial performance using effective research samples from 102 listed fishery companies. The results indicate that the linkage of multiple factors influences the improvement of fishery financial performance. This is consistent with the underlying logic of the TOE framework.

A single factor does not drive enterprises’ high level of financial performance. Still, it results from the combined action of multiple factors within the internal and external dimensions. No element may necessarily become sufficient for a company to achieve high financial performance. The path for enterprises to achieve high financial performance is not the opposite of low financial performance. Having a certain driving factor can help enterprises achieve high financial performance, but not having this driving factor does not necessarily lead to the inability of enterprises to achieve high financial performance. This also verifies the combination, equivalence, and asymmetry of causal relationships in the QCA method.

Company size is the core and necessary condition for listed fishery enterprises to achieve high financial performance. Regardless of the combination, appropriate asset size is an indispensable condition for enterprises to achieve high financial performance, and the expansion of assets is of great significance for fishery-listed enterprises to improve their returns. Enterprises should clarify managers’ responsibilities and improve asset investment and management.

Technology is an important factor in developing fishery enterprises, and digital technology plays a core or peripheral role in the three configuration paths. The results indicate that digital transformation is beneficial for improving financial performance; even in companies with unreasonable capital structures and significant debt ratios, digital transformation can still play a role. Our research conclusions are similar to previous studies, showing that the successful application of digital technology in fisheries can enhance financial performance. Additionally, a survey of small-scale fisheries in Namibia found that digital financial tools, as part of digital technology, can enhance the economic stability of fishers, thus improving financial performance.36 By comparison, it was found that digital transformation has a positive effect on the financial practices of fisheries in different countries, indicating the generality and robustness of our research conclusions.

What differentiates this study from previous ones is that it selected Chinese-listed fishery companies as research samples, further expanding the sample range. Additionally, this study explores the mechanisms of digital transformation and other variables from a configuration perspective, further elucidating the elements involved in improving financial performance through digital transformation.

External attention has a supportive role in promoting the financial performance of fishery companies. Previous research has pointed out that external attention can improve corporate performance but has not specifically discussed its role in the fishery sector.37 Furthermore, our research findings indicate the limited role of external attention in the financial performance of fisheries. Listed fishery companies cannot achieve high financial performance solely through high external attention; comprehensive measures, including internal governance, are required to enhance the performance of fishery companies.

Discussion

Marginal contribution

The possible marginal contributions of our research are as follows:

Firstly, in this paper, we try to introduce the dynamic QCA method into the research system of fishery economy. This enriches the configuration theory research of vertical sets and expands the application scope and application of QCA in research problems. This has important reference significance for promoting the development of dynamic configuration theory.

Second, previous studies mostly used quantitative or qualitative methods to study the fishery economy. This paper introduces the QCA method and adopts a new way to solve the problems of fishery enterprises, which not only helps to reveal the different mechanisms and models of fishery financial performance but also broadens the perspective of fishery research.

Thirdly, this study constructs a structural analysis framework of influencing factors of fishery financial performance. The framework deeply studies the coupling and matching relationship between preconditions, thus clarifying the complex dynamic causal relationship behind financial performance, which enriches the exploration of the relationship between variables and the mechanism of action in the model.

Management inspiration

From the fisheries enterprises’ perspective, their financial performance improvement is influenced by the synergy of multiple factors. Fisheries enterprises should choose suitable development paths based on their own conditions. In situations with limited resources, they should concentrate on their advantages and promote the development of core elements through scientific strategic deployment to enhance performance. Centralization and scale expansion are crucial for improving the financial performance of listed fisheries enterprises. Financial goal consistency can be ensured by strengthening centralized management, coordinating internal resources, and achieving unified command. At the same time, rational asset investment and scale expansion are necessary means to improve financial returns. Investments should be made based on actual conditions to avoid unnecessary waste. Additionally, external conditions and technological factors also play a key role in the financial performance of enterprises. Companies should enhance their technological capabilities, actively participate in the wave of digital transformation, and promote the development of smart fisheries. Expanding marketing channels, enhancing brand strength and awareness, attracting more external attention, and creating favorable conditions for financing and revenue are crucial for improving financial competitiveness.

Investors should focus on the multiple driving factors of an enterprise’s financial performance and assess whether the enterprise has chosen suitable development paths based on its own conditions. Investors should prioritize enterprises that can concentrate their advantages and promote the development of core elements under limited resources, as these enterprises have greater potential to improve financial performance. Additionally, investors should pay attention to whether the enterprise has scientific strategic deployments, particularly in resource allocation and core element development, which are crucial for long-term financial returns.

Supply chain partners should value establishing cooperative relationships with enterprises with conditions for centralization and scale expansion. Such enterprises have greater resource coordination and management advantages, ensuring cooperative relationships’ stability and profitability. Furthermore, partners should focus on enterprises’ digital and technological advancements. Fisheries enterprises participating in digital transformation are often more competitive, which can also benefit their partners.

In policy formulation and industry regulation, the government can refer to the findings of this study to promote the development of fisheries enterprises. Firstly, the government can formulate policies that support enterprises’ digital transformation, encouraging them to enhance their technological capabilities and participate in the wave of digital transformation, thereby promoting the development of smart fisheries. This helps improve enterprises’ financial performance and facilitates the modernization of the entire fisheries industry. Secondly, the government should encourage fisheries enterprises to expand marketing channels, enhance brand strength, and increase visibility. This can be achieved by providing market promotion subsidies, organizing industry exhibitions, and facilitating international trade connections, helping enterprises attract more external attention, promote financing and revenue growth, and enhance their competitiveness in the financial market.

Research deficiency and future prospects

This paper only uses normative qualitative comparative analysis to study fishery financial performance. Traditional research in the field of corporate governance is mostly regression or structural equation models, and future research can be verified by using both traditional empirical methods and the QCA method simultaneously.

Secondly, due to data availability limitations, this study selected annual cross-sectional financial data from 102 listed fishery companies, excluding information from quarterly and monthly reports. This limitation reduces the analytical precision in testing complex causal relationships. If researchers can collect richer sample data, they might consider employing the QCA dynamic panel r egression method to conduct similar studies, thereby enhancing the accuracy of causal inference.

The research sample for this study consists of fishery and aquaculture companies listed in China. Although these companies can partly reflect the overall state of fishery financial management, they might not accurately represent the financial issues faced by small fishery companies and individual aquaculture farmers. However, Non-listed companies’ financial data are often confidential, making it difficult for researchers to obtain accurate and fair data. Researchers can collect accurate financial data through field surveys. Additionally, small and medium-sized companies often lack standardized annual reports, making text analysis impractical for calculating their degree of digital transformation. Instead, scale methods and indicator methods should be prioritized. These approaches can help scholars conduct research focused on or combined with samples from aquaculture farmers and small-scale fishery companies. Future studies can also expand the sample range to include samples from other regions and countries, testing the applicability and heterogeneity of this study’s conclusions.

Acknowledgments

This research was funded by the “National Social Science Foundation of China: 22BGL274”;and the Collaborative Education Program of the Ministry of Education:Construction of Financial Technology Digital Intelligence Laboratory (No.220601065244932)

Authors’ Contribution

Conceptualization: Siyuan Zhang (Lead). Methodology: Siyuan Zhang (Equal), Shiwei Xu (Equal). Formal Analysis: Siyuan Zhang (Equal), Shiwei Xu (Equal), Xuping Huang (Equal). Investigation: Siyuan Zhang (Equal), Xuping Huang (Equal), Yiqi Wang (Equal). Writing – original draft: Siyuan Zhang (Lead). Funding acquisition: Siyuan Zhang (Equal), Shiwei Xu (Equal), Xuping Huang (Equal). Writing – review & editing: Shiwei Xu (Lead). Supervision: Xuping Huang (Lead).

CONFLICT OF INTEREST

The authors declare that they have no conflicts of interest.

Data Availability Statement

The data supporting this study’s findings are available from the corresponding author upon reasonable request.