Introduction

In recent years, China’s economy has developed rapidly. Faced with changes in the global economy and new challenges at home and abroad,1 China has gradually sought higher-quality development and put forward the concept of high-quality development.2 Economic development is reflected in all aspects, and agriculture is one of them. Agriculture has always been an industry that China attaches great importance to, and fishery is an important part of agriculture. Its development plays an important role in the overall development level of agriculture, and at the same time, the development of fishery also promotes the progress of rural revitalization.3 In recent years, China’s fishery economy has developed significantly.4 Figure 1 shows the change in China’s total fishery output value in the ten years from 2014 to 2023, as released by the National Bureau of Statistics of China. It can be seen that the total fishery output value has been rising in the past ten years, indicating that China’s fishery economy is also rising. However, with the deepening of economic globalization and regional economic integration, fishery development is also facing some challenges, and the connection between fishery and national strategic interests is getting closer and closer.5 Therefore, while the absolute value of the total output value of the fishery economy is increasing, it is more important to find new driving forces to stimulate the development advantages and competitiveness of the fishery economy.

.png)

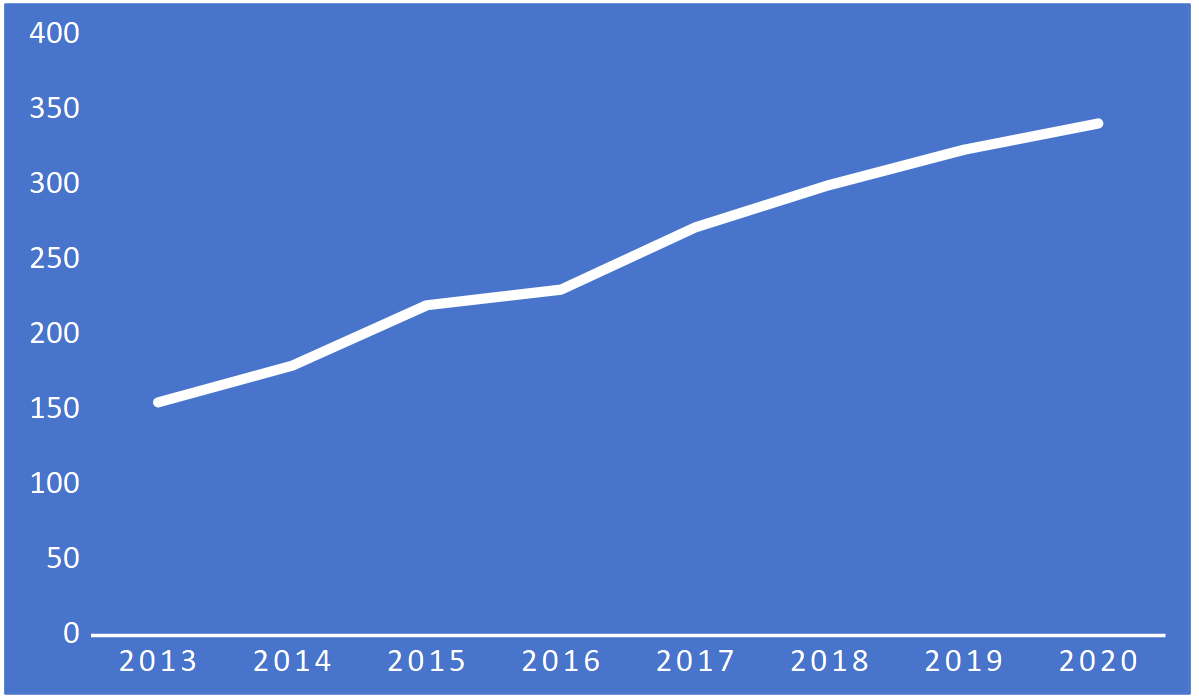

With the evolution of the global economic situation, the digital economy has gradually become a central field and gradually deepened and expanded its intersection with different fields.6 Digital finance is the product of this intersection. Digital finance is an emerging industrial form that integrates advanced digital technology with financial services,7 and it endows traditional finance with digital transformation through the digital economy. As the inclusion of digital finance gradually puts forward, the rapid development of China’s digital finance has affected many aspects of social and economic development.8 In recent years, China’s economy has transformed from the traditional resource-based economic growth model to the technological innovation-oriented economic growth model.9 The emergence of digital financial inclusion will undoubtedly promote this transformation. With the widespread adoption of mobile payment platforms, mobile payment platforms have become more efficient and convenient, and the integration of fintech with various fields has improved productivity and innovation and promoted economic growth.10 From the data in Figure 2, from 2013 to 2020, The provincial average of China’s digital inclusive finance index is rising, indicating that China’s digital inclusive finance is developing well. Combined with the data in Figure 1, there seems to be a correlation between digital financial inclusion and the growth of the fishery economy. Due to the challenges faced by the development of the fishery industry, digital inclusive finance may provide new development momentum. Then, can digital inclusive finance promote the development of the fishery economy? What is the mechanism of its influence? This is exactly the work to be studied in this paper.

The innovations of this paper are as follows: First, it links the emerging digital inclusive finance with fishery development and explores the new driving force of fishery development. As far as we know, this is one of the few studies that have applied digital inclusive finance to fishery development. Second, the role of the digital economy is highlighted in the study, and the impact of the digital level of finance on the development of fisheries is explored. At the same time, this paper has some shortcomings. The influence mechanism of digital inclusive finance on fishery development is not deeply discussed in this paper, which is the future improvement of this paper.

The overall framework of this paper is as follows: this part is the introduction to the whole paper, introducing the relevant background and leading to the work done in this paper; the second part puts forward the research hypothesis of this paper through the review of relevant literature and the sorting out of theoretical research; the third part selects relevant data and builds the econometric model; the fourth part analyzes the model results; the fifth part summarizes the conclusion of the whole paper and makes a discussion.

Literature review and research hypothesis

Literature review

At this stage, studies on the relationship between digital inclusive finance and the development of fishery economy are relatively scarce. Previous studies mainly focus on the impact of digital inclusive finance and the influencing factors of the development of fishery economy.

On the one hand, studies on the impact of digital inclusive finance on the development of the fishery economy are still relatively lacking for the time being. However, some scholars have studied the impact of digital inclusive finance on agricultural development and found that the inclusion of digital finance has brought new opportunities for the development of agriculture, rural areas, and farmers (Kun S et al.,2022).11 Among which, the analysis based on China’s situation mainly includes: On the one hand, improving agricultural green total factor productivity (AGTFP) is the key to achieving sustainable agricultural development and enabling agricultural modernization, and the development of digital inclusive finance has a direct promoting effect on local AGTFP (Li R et al.,2024; Li H et al.,2023).12,13 On the other hand, digital finance can reduce information asymmetry and farmers’ financing costs, thus reducing financing difficulty and expensive financing costs and ensuring the smooth progress of agricultural production by timely lending. The agricultural activities of farmers are directly reflected in the regional agricultural GDP, which means that the extensive development of digital finance will promote the development of the agricultural industry (Su X & Chen H,2021).14 In addition, digital finance can significantly improve the agricultural productivity of large-scale farmers (Tang Yu, 2022).15 Digital finance also plays a key role in solving agricultural enterprises’ investment and financing challenges (Shao F et al.,2024).16

On the other hand, scholars around the world have found some factors affecting the development of the fishery economy based on the data of different countries, mainly including: First, environmental factors have always been considered as important factors affecting the development of the fishery economy (Long C et al.,2022),17 among which social and environmental problems such as climate change, pollution and habitat destruction have posed severe challenges to the development of fishery economy (Moore T N,2017).18 In particular, climate change and its impact on fishery is a key issue facing fishery countries (Suh & Pomeroy R,2020),19 while the Marine environment is the material basis for the survival and development of fishery resources, and the change of the Marine environment affects the fishery economy (Yang L et al.,2022).20 Studies from Europe have found that ocean changes have a certain impact on the development of European fisheries (Anonymous, 2014).21 As an important part of the fishery economy, Marine fisheries will be subject to the positive mutual promotion effect of fishermen’s fishery investment (Xu B,2024).22 Ramczyk M (2017) introduced the research results on the impact of lake water pollution on fishery economy.23 Second, based on relevant data from China, scholars found that greenhouse gas emissions in China showed an inverted U-shaped relationship with the total output value of Marine fisheries (Yidan X et al.,2023),24 and Marine environmental pollution in China’s coastal areas and trade of aquatic products had an inhibitory effect on Marine fishery economy (Fan L et al.,2022).25 The input capacity of the fishery economy is significantly higher than the output capacity of the fishery economy. The driving effect of fishery economic input ability on fishery economic output ability is from strong to weak. The speed gradually decreases (Yu L et al.,2020).26 Third, some scholars have noticed and discussed the issues related to fishery economic management in the development of fishery (Anderson G L,2020; W. C & R. G M,2017),27,28 in which improving fishery economic performance is a common management goal. Studies have found that acquiring economic information will affect the economic performance of fisheries (Pascoe S et al.,2019).29 Some scholars have explored the relevant factors affecting the development efficiency of fisheries from the perspective of environmental constraints and proposed relevant countermeasures (Zheng L et al.,2019).30 Some scholars made early attempts to incorporate capital and investment theory into fishery economics, which has a certain reference value for managing the fishery economy (Clark W C & Munro R G, 2017).31

In addition, with the development of science and technology, scholars have gradually noticed the impact of emerging science and technology on the development of the fishery economy and have done relevant research. The main research results include the following: On the one hand, marine remote sensing technology can realize long-term, large-scale, and high-precision synchronous monitoring of marine information. Therefore, more and more applications have been applied to the research of fishery distribution and fishery environment monitoring, which plays an important role in fishery development (Peng B, 2019).32 On the other hand, informatization is a dynamic development process of using information technology to promote information exchange and knowledge sharing in all aspects of social life, which is crucial to the development of fisheries (Jianyue J & Yanming L,2021).33

To sum up, scholars have explored some influencing factors of fishery development, most focusing on Marine fishery development. At the same time, some scholars have noticed the role of digital inclusive finance in agricultural development, but there is still a lack of research on the impact of digital inclusive finance on fishery development. The research in this paper can make up for this gap to a certain extent.

Research hypothesis: The impact of digital financial inclusion on the development of the fishery economy

This paper studies the situation of China, so this part mainly focuses on the research results based on the situation of China. Studies on the impact of digital inclusive finance on the development of the fishery economy are still lacking at this stage, but existing studies have shown that the rapid development of digital technology has brought new opportunities for agricultural development (Cao L & Wang G,2024).34 The digital economy is important in promoting the high-quality and sustainable development of the Marine fishery economy (Jiang Y et al.,2024).35 With the development of the digital economy, digital finance comes into being. The emergence of digital finance has introduced innovative methods and solutions to the challenges in agricultural development (Jiang Y et al.,2024).36 With the continuous development of digital finance, the concept of inclusive finance is gradually receiving more attention. Inclusive finance and digital finance go hand in hand, helping to strengthen agricultural activities (Zubair M M. 2024),37 which makes more and more scholars combine digital financial inclusion with agricultural development for research. Especially in the context of digital agricultural development, digital financial inclusion plays a more prominent role. Digital agricultural methods and other technological improvements must be combined with financial technology as a key path. The tradeoff between resource use and profitability can be reduced, thus supporting the development of sustainable agricultural models (Sharma A et al.,2024).38 Research finds that digital financial inclusion can significantly promote high-quality agricultural development and enhance the resilience of agricultural economic development (Feng J & Wang Y,2024; Gao Q & Sun M,2024),39,40 and digital inclusive finance can break financial barriers and promote the green development of rural agriculture (Guo J et al.,2024).41 As an important part of the agricultural economy, the emergence of digital inclusive finance also brings new opportunities for fishery development. Existing studies have found that the inclusive reform of rural finance in the eastern coastal areas can promote the fishery economy (Wu Y et al.,2020).42 However, no scholars have systematically studied whether digital inclusive finance can affect the development of the fishery economy. According to the existing research results, we can speculate that there is a certain relationship between digital financial inclusion and the development of the fishery economy. Therefore, based on existing theoretical facts, this paper proposes the following hypothesis:

Hypothesis 1(H1): Digital financial inclusion can promote the development of China’s fishery economy

Research hypothesis: The regulatory effect of industrial structure upgrading in digital inclusive finance on the development of the fishery economy

With the continuous development of the economy, the upgrading and adjustment of industrial structure has increasingly become the focus of economic development of various countries (YangC et al.,2024).43 The change in industrial structure will profoundly impact national economic growth (Krüger J J, 2008),44 and many aspects influence the upgrading of industrial structure. The development of finance has a certain impact on upgrading industrial structure (Yuan M et al.,2024).45 Previous studies have shown that the development of green finance can significantly promote the upgrading of industrial structures (Xu T et al.,2024).46 As a new financial service model, digital finance can significantly promote the upgrading of industrial structure (Li W et al.,2024; Shen H et al.,2024).47,48 As the inclusion of digital finance is gradually mentioned, scholars have found that digital inclusive finance positively impacts the optimization and rationalization of industrial structure (Fei L et al.,2022).49 The upgrading of industrial structure also plays a certain role in the development of the fishery economy, which can play an intermediary effect in the impact of financial development on the growth of the Marine fishery economy (Meng Z et al.,2024).50 Based on the review of relevant theories, digital inclusive finance can promote the upgrading of industrial structure, which in turn has an impact on the development of the fishery economy. Thus, this paper proposes the following hypotheses:

Hypothesis 2(H2): Industrial structure upgrading plays a moderating role in the impact of digital financial inclusion on the development of China’s fishery economy

Research hypothesis: The regulatory role of technological innovation in digital inclusive finance on the development of the fishery economy

Digital finance and technological innovation are an important part of the high-quality development of China’s economy (Wang W & Dong Y,2024),51 although it is widely recognized that digital finance itself is the product of technological innovation. However, the development of finance will also promote technological progress (Xinyue W & Qing W,2021),52 and digital finance can promote technological innovation by providing alternative capital sources (Mou Y,2024; Chen W et al.,2024),53,54 especially innovation in digital technology (He Q & Jiang H,2024).55 The regulatory role of technological innovation in digital financial inclusion on developing the fishery economy can be discussed from two perspectives. On the one hand, developing digital inclusive finance will promote technological innovation, and existing studies have found that digital inclusive finance will significantly promote regional green technological innovation (Sun H et al.,2024).56 On the other hand, technological innovation will play an intermediary role in promoting agricultural development through digital inclusive finance (HONG L J & ZHOU J J,2024).57 Based on the review of relevant research results, digital financial inclusion promotes technological innovation, affecting agricultural development. Therefore, this paper proposes the following hypotheses:

Hypothesis 3(H3): Technological progress plays a moderating role in the impact of digital financial inclusion on the development of China’s fishery economy

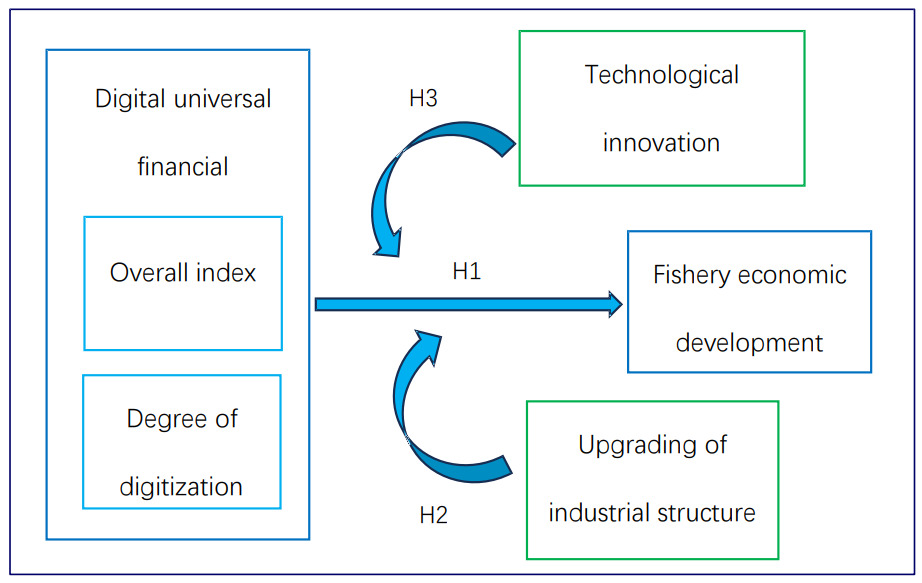

Figure 3 represents the theoretical analysis framework of this paper based on the above research hypotheses.

Research design

Data source

The data used in this paper are macro data, and the data on digital inclusive finance comes from the Digital Inclusive Finance Index (2011-2020) released by the Digital Finance Research Center of Peking University. This index has compiled 31 provinces (municipalities directly under the Central Government, autonomous regions, and leagues) and 337 cities at or above the prefecture level in mainland China. Based on the overall data availability and scientific, the digital inclusive financial index of about 2,800 counties (county-level cities, flags, municipal districts, etc., referred to as “counties”), this paper selects provincial data from 2013 to 2020 for research.

The data used for fishery development and related variables come from the China Statistical Yearbook issued by the National Bureau of Statistics of China and the local statistical yearbooks of relevant years issued by various provinces. The statistical yearbook contains the total output value of the fishery, the added value of three industries, population characteristics, resource statistics, and other data, which provide data support for the research in this paper. A total of 8 years of data from 2013 to 2020 are selected for the study.

Variable selection and descriptive statistics: Explained variables

The explained variable in this paper is the development level of fishery in China’s provinces. To measure this development level, this paper adopts the calculation method of location entropy, which reflects the competitive advantage of an industry in a certain region.58 This paper adopts location entropy to measure the development level of fishery in various provinces, and its calculation formula is shown in formula (1).

fishery ij=fij/aijFj/Aj

Where, represents the fishery location entropy of the province in year j, is the total fishery output value of province i in year j, is the total agricultural, forestry, animal husbandry and fishery output value of province in year j, is the total fishery output value of China in year j, is the total agricultural, forestry, animal husbandry and fishery output value of China in year j.

Variable selection and descriptive statistics:Core explanatory variables

The core explanatory variable of this paper is the Digital financial inclusion index. The Peking University Digital Financial Inclusion Index includes the general index of digital financial inclusion. Based on the general index, the index of coverage breadth, use depth, and digitization degree of digital financial inclusion are also compiled from different dimensions. As well as sub-indexes of payment, insurance, monetary fund, credit service, investment, credit, etc. This paper selects the total index of digital inclusive finance and the degree of digitalization as the core explanatory variables of this paper to discuss the impact of digital inclusive finance on the development of fisheries and emphasizes the role of digital development. In this paper, the total digital financial inclusion index and the digital degree are divided by 100 to introduce the model.

Variable selection and descriptive statistics: Moderator variables

In order to study the relevant mechanism of the impact of digital inclusive finance on the development of the fishery industry, this paper selected the adjustment variables from the two perspectives of industrial structure upgrading and technological innovation. Many scholars have different algorithms for the measurement of industrial structure, and this paper uses the ratio of the added value of tertiary industry to the added value of secondary industry for measurement. For the measurement of technological innovation, this paper adopts the ratio of the number of authorized patent applications and the number of accepted patent applications of each province in the current year and multiplies it by 100, that is, the proportion of successful patent application authorization (%) to measure technological innovation.

Variable selection and descriptive statistics: Control variables

According to Cobb-Douglas production function, output will be affected by capital, labor, and other factors, and economists often believe that government intervention, consumption, and other factors will affect economic development. Therefore, based on the production function and related theories, this paper combines relevant existing theoretical studies. Population density (person/square kilometer), urban registered unemployment rate (%), retail price index of aquatic products (last year =100), general budget expenditure of local finance (100 million yuan), and consumption level were selected as control variables. Population density and urban registered unemployment rate reflected the labor factor. Local general budget expenditure reflected the capital factor and government intervention factor. The retail price and consumption level of aquatic products reflects the influence of consumption. Among them, consumption level is measured by the ratio of per capita consumption expenditure to per capita GDP. Meanwhile, in order to eliminate dimensional differences between data, logarithmic processing of population density and local general fiscal expenditure is introduced into the model, and the retail price index of aquatic products is divided by 100 to introduce the model.

Descriptive statistics of variables

Table 1 shows the descriptive statistics of the variables used in this paper. Among them, the minimum value of the location entropy of the fishery economy is only 0.007, while the maximum value is 3.487, indicating that there is a large gap between the location entropy of different regions in different years. For the index of digital inclusive finance, there is a large difference between different regions, whether the total index or the degree of digitalization. Most of the control variables also have large differences. The minimum value of population density is 2.64, and the maximum value is 3925; the gap between the registered urban unemployment rate is small, with a minimum value of 1.2 and a maximum value of 4.6; the retail price index of aquatic products is between 95 and 110; and the minimum value of the general budget expenditure of local finance is 922.48. The maximum value is 17,430.79, indicating that different regions have different levels of government financial support. The minimum value of consumption level is 0.216, and the maximum value is 0.458, with a certain gap.

Model construction: Baseline regression model

In this paper, the benchmark regression to examine the impact of digital financial inclusion on the development of China’s provincial fishery economy is constructed as formula (2). Since the used data are panel data, the use of the random effect model and fixed effect model is selected through the Hausman test during the empirical test.

Yi=α1+α2Xi+α3Ci+εi

Where is the explained variable, is the intercept term, and is the coefficient to be estimated, is the core explanatory variable, is the control variable, and is the random disturbance term. After the Hausman test, if the model chooses the fixed effect, the dual fixed effect model is used; that is, the individual and time are controlled, and the individual and time fixed effect terms are introduced into the model.

Model construction: Moderating effect model

In order to study the regulatory role of technological innovation and industrial structure upgrading in the impact of digital inclusive finance on the development of fishery economy, this paper constructs a moderating effect model and introduces interactive terms into the benchmark regression, as shown in formula (3).

Yi=β1+β2Xi+β3Ri+β4Xi×Ri+β4Ci+εi

Where is the regulating variable, and is the interaction term between the core explanatory variable and the regulating variable. To prevent collinearity, the variables are decentralized when calculating the interaction term, and other models are set in accordance with the baseline regression. At this time, the main concern is the positive and negative and the significance of the coefficient

Model construction: β convergence model

The calculation of spatial or regional economic convergence process is an important part of econometrics (Kosfeld R & Lauridsen J,2004).59 To test the impact of digital inclusive finance on the convergence of regional fishery economic development, this paper introduces a convergence model for testing, and its model is set as follows:

Yit=δ1Yit−1+γit+πit

Yit=λ1Yit−1+λ2Yit−1×Xit−1+λ3Cit−1+γit+πit

Where is the lag of the explained variable of the first order, is the lag of the core explanatory variable of the first order, is the interaction of the explained variable of the first order and the core explanatory variable of the first order, and is the parameter to be estimated, is the lag of the control variable of the first period, other definitions are the same as above. (4) is the general convergence model, that is, the model without introducing explanatory variables. Inter-regional fishery economic development convergence can be judged according to the positive and negative values If the value is significantly negative, it indicates that there is convergence of inter-regional economic development. In model (5), the convergence of explanatory variables is introduced.

According to the positive and negative coefficient of the interaction term theconvergence impact of digital inclusive finance on the development of the regional fishery economy can be judged to be significantly negative. It shows that digital inclusive finance will promote the convergence of the development of the inter-regional fishery economy; on the contrary, it will inhibit the convergence.

Correlation analysis

Table 2 shows the Pearson correlation test results among the main explained variables, core explanatory variables and moderating variables. The correlation coefficients and significance in the table show that the correlation coefficients among most variables are significant at the significance level of 1%, indicating that there is a strong correlation between the main variables. However, the specific influence relationship needs to be further tested by the econometric model.

Empirical results and analysis

The impact of digital financial inclusion on the development of the fishery economy

Table 3 is the result of baseline regression, columns (1) and (2) in the table are the result of the impact of digital financial inclusion on the development of the fishery economy, columns (3) and (4) are the result of the impact of digital degree on the development of fishery economy, and columns (1) and (3) are the result of the model without adding control variables. Columns (2) and (4) are the results after the addition of control variables. The Hausman test is significant at the selected significance level, indicating that it is appropriate to select a fixed-effect model. From the coefficient, whether the control variables are added or not, digital inclusive finance and the degree of digitization positively impact the development of the fishery economy at the significance level of 1%. It shows that the development of digital inclusive finance and digitalization can promote the development level of the fishery economy in each province, and hypothesis 1 is verified.

In addition, some control variables will also have a significant impact on the development level of the fishery economy. Unemployment will inhibit the development level of the fishery economy in each province at the significance level of 5%, and the general budget expenditure of local finance will promote the development of the fishery economy at the significance level of 1%, which is basically consistent with the situation shown by the Cobb-Douglas production function. Population density and consumption level will have a positive impact on the development of the fishery economy, but the result is not significant. This result is consistent with most previous studies. The result of the model can provide a reference for the countermeasures to promote the development of the fishery economy from the perspective of digital finance.

Results of the endogeneity test and robustness test

To solve the possible result bias caused by the endogeneity problem, this paper uses the system generalized moment estimation method (SYS-GMM) to conduct the endogeneity test and introduces the one-stage lag of the explained variable into the model as the explanatory variable. The results are shown in columns (1) and (2) of Table 4. Columns (1) and (2) in the table are the endogenous test results of the total index of digital inclusive finance and the degree of digitization, respectively. From the results of column (1) in the table, the P value of AR(1) is less than 0.1, and a P value of AR(2) is greater than 0.1, indicating that the model setting can avoid residual autocorrelation. The P values of the Sargan test and Hansen test are both greater than 0.1, and the null hypothesis cannot be rejected, indicating that there is no over-recognition of instrumental variables and the model construction is effective. The results in column (2) of the table show that the P value of AR(1) is less than 0.1, and that of AR(2) is greater than 0.1, indicating that the model setting can avoid residual autocorrelation. The results of the Sargan and Hansen tests show no over-recognition of instrumental variables, so the model construction is correct. In addition, the correlation coefficients are also significant, so the robustness test results show that the construction of the benchmark regression model is basically correct.

After the endogenous test, a robustness test is needed to further verify the robustness of the model. This paper carries out the robustness test from two perspectives: First, change the measure of explained variables, replace the total output value of agriculture, forestry, husbandry, and fishery in the formula of location entropy with the added value of primary industry, and calculate the changed explained variable Fishery_C; The second is to replace the core explanatory variables and use the lag of the core explanatory variables to set the model. The results of the robustness test are shown in columns (3) to (6) of Table 4. From the results of the Hausman test, it is correct to choose the fixed effect model, and columns (3) and (4) are the results after replacing the explained variables. At this time, the total index of digital inclusive finance and the degree of digitalization are still at the significance level of 1% and positively promote the development of the fishery economy. Columns (5) and (6) are the results after changing the core explanatory variables, and the results show that the total digital financial inclusion index and the one-stage lag of the digitalization degree have a positive impact on the development of fisheries at the significance level of 1%. The results of robustness test show that the construction of baseline regression is robust.

Adjustment effect analysis

Table 5 shows the model results of the regulatory effect. Columns (1) and (2) in the table show the regulatory effect of technological innovation. The results in column (1) show that the interaction item between technological innovation and digital inclusive finance positively affects the development of the fishery economy at the significance level of 5%. In other words, technological innovation plays a positive regulating role in the impact of digital inclusive finance on the development of fishery economy. The interaction item between technological innovation and digitalization level in column (2) is significant at the significance level of 1%, indicating that technological innovation plays a positive regulating role in the impact of digital inclusive finance digitalization degree on the development of fishery economy. Therefore, hypothesis 3 is confirmed. This result is also consistent with the effect of technology on economic growth in economic growth theory.

In the table, columns (3) and (4) are the results of the adjustment effect of industrial structure upgrading, column (3) is the adjustment effect of industrial structure upgrading on the total index of digital inclusive finance, and column (4) is the adjustment effect of industrial structure upgrading on the digitalization degree of digital inclusive finance, and the interaction terms of the two columns are significantly negative at the significance level of 1%. This indicates that the upgrading of industrial structure plays a negative regulating role in the impact of digital inclusive finance on the development of fishery economy, that is to say, the upgrading of industrial structure will inhibit the promoting role of digital inclusive finance on the development of fishery economy. It may be because this paper focuses on upgrading the industrial structure to increase the proportion of the tertiary industry, which itself is unfavorable to the primary industry. Which is consistent with the research conclusion of Bo W et al. (2021). This study believes that the progressive evolution of industrial structure is unfavorable to the development of fishery economy,60 which verifies the results of the regulatory effect in this paper. Based on this result, hypothesis 2 is proved.

Analysis of regional economic convergence

Table 6 shows the model results of β convergence. The first is β convergence result, and the lag coefficient of location entropy of fishery economy is positive at the significance level of 1%, indicating that there is no convergence of fishery economic development level among provinces. Columns (2) and (3) are conditional β convergence results after adding the total index of digital inclusive finance and the degree of digitalization. From the perspective of the coefficient of the interaction term, the coefficient of the interaction term of the two models is positive at the significance level of 1%, indicating that whether it is the total index of digital inclusive finance or the degree of digitalization, the development of digital inclusive finance will widen the gap in the development of fishery economy among regions, that is to say, digital inclusive finance will play a more obvious role in promoting the development of regions with a higher level of fishery development. This conclusion can provide a reference for the coordinated development of an inter-regional fishery economy based on a financial perspective.

Conclusion and discussion

Conclusion

This paper uses the panel data of 31 provinces, municipalities, and autonomous regions in China during a total of 8 years from 2013 to 2020, to empirically analyze the impact of digital financial inclusion on the development of the fishery economy, and mainly draws the following conclusions:

First of all, the benchmark regression results show that the development of digital inclusive finance will significantly promote the development of regional fishery economy, whether in terms of the total index level or the degree of digital development, and some control variables selected based on the Cobb-Douglas production function will also have an impact on the development of fishery economy. After the robustness and endogeneity tests of the system GMM model, the results are still significant, indicating that the model results are credible.

Secondly, the moderating effect model shows that technological innovation plays a positive moderating role in the impact of digital inclusive finance on the development of the fishery economy, while the upgrading of industrial structure is not conducive to the promotion of digital inclusive finance on the development of the fishery economy, and the upgrading of industrial structure plays a negative moderating role in its impact.

Finally, the results of the general β convergence model show that there is no convergence in the development of fishery economy among provinces and regions, that is to say, the development level of fishery economy in various regions is gradually expanding, while the conditional β convergence model shows that digital inclusive finance has a greater role in promoting regions with higher development level of fishery economy. Therefore, the development of digital inclusive finance will widen the gap in the development level of the fishery economy in different regions.

Discussion

The research conclusions of this paper can provide valuable conclusions for solving the problem of provincial fishery economic development in China. Past scholars rarely paid attention to the correlation between digital inclusive finance and fishery economic development. This paper verifies the impact of digital inclusive finance on fishery economic development through an econometric model. Provinces and regions can look for new ideas to develop fisheries from the perspective of digital finance.

On the one hand, it is necessary to continue vigorously promoting the development of the fishery economy and protecting natural fishery resources.61 And strengthen cooperation and exchanges among different regions. All localities can build a coordinated development system according to local conditions, learn from each other, and jointly promote the development of the fishery economy. On the other hand, digital financial inclusion can provide various support for developing the fishery economy, such as technological innovation, financial support for technical facilities, etc., which provides more possibilities for developing the fishery industry. Therefore, it is necessary to continue to promote the development of digital inclusive finance in various places, and relevant policy subsidies can be formulated, and financial education can be carried out.

There is still room for improvement in this study. The mechanism of digital inclusive finance affecting the development of fishery economies is a complex issue, and it has not been deeply discussed in this paper. In the future, with the discovery of new research, the mechanism can be more perfect so that digital inclusive finance can be better applied to the development of fishery economies.

Acknowledgments

This research was funded by “National Social Science Foundation of China: 22BGL274”.

Authors’ Contribution

Conceptualization: Lingsheng Chen (Equal), Shiwei Xu (Equal). Methodology: Lingsheng Chen (Equal), Jianli Bai (Equal). Formal Analysis: Lingsheng Chen (Equal), Shiwei Xu (Equal), Zhengrong Cheng (Equal). Investigation: Lingsheng Chen (Equal), Shiwei Xu (Equal), Jiahui Chen (Equal). Writing – review & editing: Lingsheng Chen (Equal), Shiwei Xu (Equal), Zhengrong Cheng (Equal), Jiahui Chen (Equal). Supervision: Lingsheng Chen (Equal), Shiwei Xu (Equal). Writing – original draft: Jianli Bai (Lead). Funding acquisition: Shiwei Xu (Lead).

CONFLICT OF INTEREST

The authors declare that they have no conflicts of interest.

Data Availability Statement

The data supporting this study’s findings are available from the corresponding author upon reasonable request.